What is group health insurance, and why it matter

Definition and key terms

Group health insurance is a single health policy purchased by an organisation (commonly an employer or member association) that covers a defined group of people under a master policy. The organisation is typically the policyholder (master policyholder), while individual employees or members are insured members named under that policy. Dependents—such as spouses and children—can often be included as dependents under the same policy, subject to plan limits and eligibility rules.

Key terms to know:

- Policyholder / Master policy: The employer or association that buys the group cover.

- Insured members: Employees or members covered under the master policy.

- Dependents: Family members allowed on the policy (spouse, children).

- Sum insured: The coverage limit (per member or family) for claims.

- TPA (Third-party administrator): An entity that manages claims and networks on behalf of insurers.

Group versus individual insurance

Group and individual health plans deliver similar functions—paying for healthcare costs—but they differ in underwriting, pricing, portability, and administration.

- Underwriting: Group plans are often offered with simplified or no individual medical underwriting, especially for healthy cohorts. Individual plans typically require medical history disclosures and may apply waiting periods or loadings.

- Pricing: Group premiums are pooled across members and may be cheaper per person because risk is spread. Individual premiums are set for each person based on age, health, and other risk factors.

- Portability: Individual plans stay with the person when they change jobs. Group plans are tied to the policyholder—coverage usually ends when employment ends unless conversion or portability options are offered.

Example: A 35-year-old employee might pay little or nothing for a group plan offered by their employer, while the same person buying an individual plan could pay a higher premium due to age-based pricing.

Who the policy covers

Group policies commonly cover:

- Employee-only: Coverage limited to the employee.

- Employee + family (family floater): A shared sum insured covers the employee and listed dependents.

- Employee + spouse / children / parents: Insurers may offer flexible dependent add-ons, subject to plan rules.

Eligibility rules generally require active employment (full-time) and may include probation periods (e.g.,30–90 days) before cover begins. Membership-based groups (professional associations, cooperatives) can also act as policyholders to offer group schemes to members.

How group health insurance works and who is eligible

Employer-sponsored plans explained

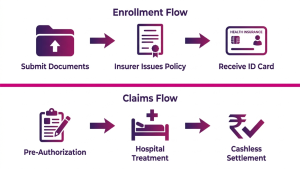

In employer-sponsored group health insurance, the employer contracts with an insurer for cover on behalf of eligible employees. The employer often pays all or part of the premium and handles enrolment administration. Insurers or TPAs provide services such as network management, claim adjudication, cashless facility setup, and member ID issuance.

Typical administrative flow:

- Employer negotiates terms (sum insured, dependents, riders, pricing).

- Employees submit enrollment forms and required documents.

- The insurer issues policy, ID cards, and member lists to the employer.

- Claims are filed via a cashless network or reimbursement procedures.

- Policy renewal occurs annually with potential rate adjustments.

Eligibility rules and waiting periods

Common eligibility rules include minimum service thresholds (e.g.,3 months), full-time status, or minimum working hours. Waiting periods are standard for specific items—new joiners may face:

- Initial waiting period: Short period before any benefits apply (rare).

- Pre-existing condition waiting period: Coverage for known medical conditions may be restricted for a defined period (commonly 12–48 months, varies by jurisdiction).

- Specific benefit waiting: Maternity and some high-cost treatments often have separate waiting periods.

When adding dependents (marriage, childbirth), insurers usually require proof—marriage certificate or birth record—and may limit enrollment windows (e.g., within 30–60 days of the event).

Policy duration and renewals

Group policies are typically annual and renew on a fixed date. At renewal, the insurer may change rates based on claims history, demographic shifts (ageing workforce), and market conditions. Mid-year changes (mergers, headcount reduction, or business acquisition) can trigger policy amendments or pro-rata premium adjustments. Employers negotiate renewals and may tender the business to multiple insurers to secure better pricing or service terms.

Types of group health insurance plans and key features

Comprehensive versus limited benefit plans

Comprehensive group plans aim to cover broad medical expenses, including hospitalisation, surgeries, diagnostics, and often some outpatient elements, subject to limits and exclusions. Limited benefit or fixed-benefit plans pay a predetermined amount for certain events (e.g., fixed cash per day of hospitalisation) and are used where predictability or cost-control is a priority.

Typical exclusions to watch for: cosmetic treatments, non-medical hospitalisation costs, elective procedures not pre-authorised, or experimental therapies.

Top-up, floater, and rider options

Employers and members can combine plan types to meet needs:

- Family floater: One sum insured shared across the employee and dependents. Efficient for younger families with low simultaneous claims.

- Top-up or super-top-up: An additional layer of cover that begins after the base plan’s threshold is exhausted—useful for high-cost events.

- Riders/add-ons: Common riders include maternity, critical illness, outpatient (OPD) coverage, dental, and vision. Employers decide which riders to include in the employer-paid core plan or offer as voluntary employee-paid options.

Network, cashless, and managed care features

Insurers maintain empanelled hospital networks where cashless authorisation lets members receive treatment without paying up-front for covered hospitalisation. Typical cashless process:

- Pre-authorisation request by the hospital to the insurer/TPA.

- Insurer/TPA verifies coverage and issues approval if eligible.

- Hospital settles with insurer; member pays only non-covered items.

Managed care features can include pre-authorisation, case management for high-cost cases, wellness programs, telemedicine, and negotiated bundled pricing with hospitals. These reduce claim costs and improve member experience.

Benefits and typical coverage in group health insurance

Inpatient and outpatient coverage

Inpatient (hospitalisation) coverage is the core benefit in most group plans and typically covers room rent (subject to sub-limits), surgeon fees, anaesthesia, diagnostics during admission, and post-hospitalisation expenses for a defined period. OPD (outpatient) coverage—consultations, diagnostics, pharmacy—may be included in some group plans or offered as a rider with limits or per-claim caps.

Examples of covered services: planned surgeries, emergency admissions, diagnostic tests during hospitalisation, and post-discharge follow-ups for a set duration (e.g.,30–90 days).

Maternity, newborn, and chronic care benefits

Maternity cover is commonly optional or subject to waiting periods. If included, it can pay for delivery costs and pre/post-natal care. Newborns are usually covered if enrolled within a specified window (often within 30–90 days of birth).

Chronic disease management—covering diabetes, hypertension, and other long-term conditions—may be part of the policy or supported through disease-management programs. Employers sometimes provide additional wellness support to help manage chronic conditions and reduce long-term claims.

Preventive care and wellness programs

Many group plans include preventive benefits such as annual health checkups, screenings, vaccinations, and wellness portals. Employers increasingly add incentives (health credits, premium discounts, or rewards) to encourage healthy behaviours. Preventive care helps detect issues early and can reduce high-cost claims over time.

Costs, premiums, and employer/employee contributions

How premiums are calculated

Group premiums are calculated using actuarial principles that consider the risk profile of the group: age distribution, past claims experience, average sum insured, geographic distribution, and industry sector. A younger workforce or a low-claims history typically attracts lower rates. Rate drivers that increase premiums include an ageing workforce, high prior claims, generous sums insured, and expanded coverage (maternity, OPD, critical illness).

Insurers may offer rate guarantees or multi-year pricing arrangements for large groups, and underwriting may be experience-rated—meaning claims history directly affects renewal pricing.

Cost-sharing and payroll deductions

Cost arrangements vary by employer:

- Employer-paid core cover: Employer pays full premium for a basic level of cover.

- Shared contributions: Employer pays a portion, and employees contribute via payroll deduction.

- Voluntary top-ups: Employees pay extra for a higher sum insured or riders.

Payroll deductions must be administered transparently, with clear communication on how much is deducted, tax treatment, and options for voluntary benefits.

Tax treatment and savings

Tax treatment of employer-paid premiums and employee contributions depends on local law. In many jurisdictions, employer-paid group health premiums are tax-deductible for the employer and tax-exempt or tax-advantaged for the employee up to certain limits. Employees should consult a tax advisor for their country’s specifics, and HR should document any tax benefits offered as part of total compensation.

Enrollment, claims, portability, and exiting a group policy

Enrollment and adding dependents

Enrollment windows are typically at hire or during an annual open enrollment. Employers usually request identity documents and proof for dependents (marriage certificate, birth certificate). Late enrolment or adding dependents outside the permitted window may be allowed only with insurer approval or during qualifying life events.

Filing claims and the cashless network process

Claims follow two main routes:

- Cashless: For empanelled hospitals, the hospital initiates pre-authorisation and, once approved, bills the insurer/TPA directly for covered items. Members may only pay exclusions or co-payments.

- Reimbursement: For non-empanelled providers, members pay upfront and submit bills and medical records to the insurer for reimbursement. This route requires careful documentation to avoid delays.

Tips to avoid claim rejections: keep receipts and discharge summaries, obtain pre-authorisation for planned admissions, and follow insurer timelines for submission. Common rejection reasons include missing documents, treatment not covered, or exceeding sub-limits.

Portability and post-exit options

Because group cover is linked to the policyholder, coverage usually ends when employment stops. Options to maintain cover after exit depend on local rules and the insurer’s offerings:

- Conversion to individual policy: Some insurers allow conversion to an individual plan without fresh medical underwriting, but possibly at a different premium.

- Continuation schemes (e.g., COBRA-like): In some countries, law or employer policy may permit temporary continuation of coverage if the employee pays the full premium.

- Portability rules: Local regulatory portability (as in some markets) may allow moving to an individual policy while retaining continuity of benefits for waiting periods.

Employees planning a job change should discuss exit timelines with HR and request documentation that proves continuity of coverage where needed for conversion or portability.

Group insurance schemes and related employee protection products

Group term life and accidental cover

Group term life insurance provides a lump-sum benefit to the nominee if an employee dies during the policy term. Cover amounts are typically fixed (e.g., a multiple of salary) or set sums. Group accidental death & dismemberment (AD&D) covers accidental death and defined disabilities, often with separate benefit schedules.

Differences vs health cover: life and AD&D pay defined benefits on occurrence rather than reimbursing medical expenses. Employers commonly bundle health, life, and accidental coverage to provide broader financial protection for employees and families.

Association and cooperative schemes

Professional associations, trade unions, or cooperatives can act as policyholders and offer group plans to their members. These schemes are useful for freelancers, small businesses, or professionals without a large employer. Governance is member-driven and eligibility, pricing, and benefits depend on the association’s negotiation power and membership demographics.

How group schemes differ from employer plans

Group schemes organised by associations often have wider membership eligibility, may be more portable between jobs, and are governed by member rules rather than employer policy. Funding, renewal negotiation, and oversight can differ—association schemes may be voluntary with direct member billing, while employer plans are employer-managed and often subsidised.

How to choose the right group health insurance plan

Compare coverage against cost

Start with a compact framework: core cover (inpatient, pre/post hospitalisation), exclusions, sum insured, sub-limits (room rent, ICU), and benefit extensions (maternity, OPD). Ask whether the plan has per-employee or family floater sums insured and whether sub-limits or co-payments apply.

Decision rule: if medical inflation or claim frequency in your organisation is rising, prioritise higher sum insured or top-up options. For younger workforces with a low claim probability, a floater may be a cost-efficient option.

Assess insurer network and claim support

Evaluate the insurer’s empanelled hospital network (coverage in key cities where employees live), TPA responsiveness, claims settlement ratio, and turnaround times. Ask prospective insurers for sample service-level agreements, a list of empanelled hospitals, and references from existing corporate clients.

Questions HR should ask insurers:

- What is your claim settlement turnaround time for cashless and reimbursement?

- How do you manage high-cost cases and pre-authorisation?

- Can you provide the employee portal and reporting dashboards?

Checklist for HR and employees

Compact checklist HR can use when selecting or renewing a plan:

- Confirm the eligible population and dependent rules.

- Compare sum insured, sub-limits, co-pay, and riders across vendors.

- Review historical claims data and expected rate changes.

- Check network adequacy for employee locations.

- Define the communication plan and the enrolment process for employees.

For employees, ask HR these 5 questions: What is my sum insured? Are my dependents covered? What are waiting periods? How does cashless work? What portion (if any) will be deducted from my salary?

Read our blog: How to Choose the Right Group Health Insurance for Your Employees

Conclusion

Group health insurance is a valuable employee benefit that balances affordability and administrative ease. Choosing the right plan comes down to matching coverage to workforce demographics, controlling long-term costs through managed care and wellness, and checking insurer service performance.

Checkout our Group Health Insurance Plan

Frequently asked questions

1. What is the difference between group and individual health insurance?

Group plans are bought by an organisation and typically have pooled pricing and simplified underwriting; individual plans are bought by individuals and priced based on personal risk factors.

2. Who is eligible for group health insurance and when does coverage start?

Eligibility usually depends on employment status and company rules; coverage commonly begins after a probation period or at hire, subject to plan waiting periods.

3. Does group health insurance cover pre-existing conditions?

Many group plans apply waiting periods for pre-existing conditions; coverage after waiting depends on the insurer’s policy and the duration of continuous cover.

4. Can I keep my group health insurance after leaving my job?

Usually no — coverage ends with employment. Options may exist to convert to an individual policy or temporarily continue coverage if the insurer or local rules allow.

5. How do cashless claims work under a group policy?

For empanelled hospitals, the hospital requests pre-authorisation from the insurer/TPA and, once approved, bills the insurer directly for covered items; the member pays only non-covered expenses.