Employers deciding whether to offer group health insurance — or advising staff who already have employer cover — need a practical, clear comparison. This guide explains how group (master policy) and individual (personal) health plans differ, the pros and cons of each for employers and employees, when a staff member should keep or buy a personal plan, and simple steps HR can use when selecting or renewing coverage.

What is group health insurance?

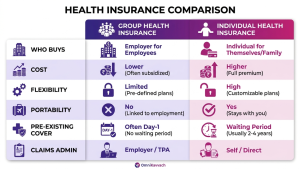

Who buys group policies?

Group health insurance is purchased by an employer, association, cooperative or other organisation to cover a defined set of members (usually employees). The insurer issues a master policy to the employer; individual members receive certificates of insurance or enrolment under that master policy. Employers typically handle premium payments, enrollment, and some administrative tasks (in coordination with the insurer or a TPA).

Who is covered under group plans?

Coverage usually includes eligible employees and, depending on the plan, selected dependents (spouse, children). Insurers often define eligibility rules: minimum service period or completion of probation, categories for permanent vs contract staff, and specific dependent limits. Employers can choose whether to include probationary or contractual employees, but uniform sums insured are common (the same cover level for a role or bracket).

Common group insurance terms

Master policy: The contract between the insurer and the employer covering the group.

TPA (Third Party Administrator): Handles claim administration and support when appointed by the insurer.

Network hospitals / cashless facility: Pre-agreed hospitals where cashless claims are processed directly with the insurer/TPA.

Day‑1 PED: Some group plans waive waiting periods for pre-existing diseases; check policy wordings for limits and exclusions.

Certificate of insurance: The individual evidence of cover for each employee under the master policy.

Check out our complete guide on Group Health Insurance—>

What is individual (personal) health insurance

Individual vs family‑floater covers

Individual health insurance policies are bought by a person (or family) and are owned by that policyholder. A single-person individual policy covers only the insured, while a family-floater policy covers multiple family members under one sum insured. Family-floater policies can be cost-efficient for young families, but the shared sum insured means a single large claim can reduce cover availability for other members.

Ownership and portability rules

Individual policies are owned and controlled by the policyholder: renewals, claim follow-ups, and portability decisions rest with them. Portability rules allow policyholders to move their individual policy to a new insurer without losing accumulated benefits (such as completed waiting periods), subject to insurer and regulator rules. Portability does not apply to group master policies; when employees leave a job, employer-provided coverage generally ends.

Pre‑policy checks and waiting periods

Insurers may require medical checks for older applicants or where high sums insured are requested. Individual plans typically impose waiting periods for pre-existing conditions (ranging from 2 to 4 years, depending on the insurer and local regulations) and specific waiting periods for maternity care or certain treatments. These differences are why portability and early purchase of personal cover can matter for employees.

Direct comparison: group vs individual — key differences

Cost and premium responsibility

Group premiums are usually paid (fully or partially) by the employer and benefit from risk pooling, resulting in lower per-employee cost. Individual premiums are paid by employees and reflect age, health and chosen sum insured — they are typically higher but tailored.

Coverage flexibility and customisation

Individual plans offer wide customisation (higher sums, riders for maternity, OPD, critical illness). Group plans are typically uniform and have limited add-ons; employers decide the baseline benefits for all members or for employee tiers.

Portability and continuity of cover

Employees lose most group cover when employment ends (unless the policy has portability/convertibility options — rare). Individual policies stay with the insured and can be ported between insurers, preserving waiting period credits.

Pre-existing condition treatment

Many group plans offer immediate or day‑1 coverage for pre-existing conditions, but exceptions and caps may apply for high-value claims or certain conditions. Individual policies usually have waiting periods for pre-existing conditions, though these are reduced when ported with documented prior coverage and claim history.

Claims process and administration

Group claims are often routed through the employer and a TPA; employers may be involved in escalation and documentation. Individual claims are managed directly between the insured and insurer (or insurer-appointed TPA), giving the policyholder full control over claim follow-up.

| Feature | Group Health Insurance | Individual Health Insurance |

| Who buys | Employer/organisation | Individual / family |

| Cost | Lower per head (often employer-paid) | Higher, paid by the individual |

| Flexibility | Limited customisation | Highly customisable |

| Portability | Usually ends on exit | Portable between insurers |

| Pre-existing conditions | Often covered day‑1 (policy terms apply) | Waiting periods typically apply |

| Claims admin | Employer/TPA managed | Policyholder manages with insurer/TPA |

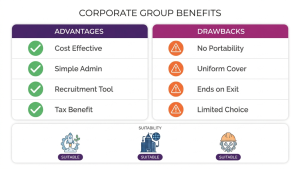

Benefits, limits and suitability of group plans

Key advantages for employers

A cost-effective way to provide basic health cover and improve employee benefits.

Simplified administration: a single master policy and consolidated renewals.

Helps with recruitment and retention — a valued employee benefit.

Possible tax or accounting benefits depending on local rules.

Common drawbacks and risks

Limited individual choice — employees may need different sums or riders.

Coverage typically ends on exit, creating portability gaps for employees.

Uniform sums can under-insure higher-risk staff or those with families.

Potential for moral hazard if plan design is not carefully managed (e.g., high utilisation).

Which organisations benefit most

SMEs and startups can use group plans to provide meaningful baseline cover at a manageable cost. Large corporations benefit from economies of scale and can design tiered benefits. For blue-collar or widely dispersed workforces, group cover is often the most practical way to offer immediate protection. Organisations that need to attract senior hires may combine group cover with allowances for personal top-ups.

When and why employers should encourage individual plans

Situations favouring individual cover

Employees who expect large future medical expenses or need higher sums insured (senior staff or extended families).

Staff approaching job transitions who need portability or continuity.

Employees with specific needs (maternity planning, chronic conditions) where tailored policies are better.

Those who prefer control over renewals, network choices or claim handling.

Using individual plans as top‑ups

Individual top-up or super top-up policies activate after a chosen deductible (threshold) is met. They’re cost-efficient when the group cover offers a base sum insured. Example: employer provides Rs.3 lakh cover; an employee buys a Rs. 10 lakh top-up with a Rs. 3 lakh deductible. Coordinate deductibles and understand whether the top-up applies per claim or aggregate.

Recommended riders and add-ons

Maternity cover — often excluded from group plans or offered with limits.

Critical illness riders — useful for defined-lump-sum payouts.

OPD, dental and preventive care riders — frequently absent in group policies.

Personal accident coverage — complements medical hospitalisation benefits.

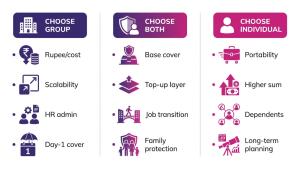

When to Choose What?

Choose Group Health Insurance When

- You want to provide employees with affordable health coverage at a lower per-person cost.

- Your business needs a scalable employee benefit without heavily increasing payroll expenses.

- Administrative simplicity is important, and HR prefers one master policy instead of multiple individual plans.

- You want immediate insurance access for employees, including possible Day-1 pre-existing condition coverage.

- You are using health benefits to improve hiring, retention, and employee satisfaction.

- Your company has a large or growing workforce that benefits from pooled risk pricing.

- You need a practical baseline healthcare benefit for blue-collar, field, or distributed teams.

Read the complete guide on How to Choose the Right Group Health Insurance for Your Employees —>

Choose Individual Health Insurance When

- You want coverage that continues even if you resign, switch jobs, or take a career break.

- You need a higher sum insured than your employer plan provides.

- You have dependents such as a spouse, children, or parents needing stronger protection.

- You want policy features like maternity, OPD, dental, critical illness, or accident riders.

- You prefer direct control over renewals, claims, and insurer choice.

- You are planning long-term and want the waiting periods completed early.

- You do not want to depend entirely on your employer for healthcare security.

Choose Both Together When Possible

- You want the employer plan as base coverage and a personal policy as extra protection.

- You need higher total coverage at a lower cost than buying a large standalone policy.

- You want protection against sudden job loss or career transitions.

- You want to reduce out-of-pocket medical risk during major hospitalisation.

- You want better financial security for family responsibilities.

- You want the smartest balance between affordability and long-term continuity.

What Employers Should Do

- Use group insurance as the default employee benefit.

- Review whether the sum insured is realistically enough for employees.

- Offer tiered plans if workforce needs vary widely.

- Educate employees on the limits of group cover and exit-related risks.

- Encourage personal top-up or individual plans for those needing more protection.

When Employees Don’t Read Their Health Policy—>

Conclusion

For employers, group health insurance is a cost-efficient baseline benefit that simplifies administration and improves employee satisfaction. Individual policies offer portability, customization and continuity. The best approach for many organisations is to provide a thoughtful group plan (possibly tiered) while educating and encouraging employees to maintain or buy individual plans as top-ups where needed. Use the checklists above during selection, communicate clearly with staff about limits and exit rules, and consider broker support to negotiate favourable terms and service SLAs.

Explore Our Group Health Insurance Plans—>

FAQs

1. Can I keep my individual policy if my employer gives group cover?

Yes, you can hold both. Many employees keep an individual policy for continuity and top-up purposes; the individual policy remains active, and claims can be coordinated depending on policy terms.

2. What happens to group health insurance when I leave my job?

Group cover typically ends on exit or on the policy renewal date. Some employers offer conversion options for a fee; otherwise, employees should port or buy an individual policy to avoid gaps.

3. Are pre-existing conditions covered under group insurance?

Some group plans offer day‑1 coverage for pre-existing conditions — check policy terms. Coverage may have limits or exclusions for certain conditions and high-value claims.

4. Is it worth buying a top-up policy in addition to group cover?

Often, yes, top-ups are cost-effective to increase overall cover beyond the group sum insured. Assess expected risk, out-of-pocket limits and deductible mechanics before buying.

5. Who is responsible for filing claims under a group policy?

Claims can be filed by the employee, but are often administered via the employer or appointed TPA. HR should clarify the internal process, documents required and contact points.