Corporate health insurance, often referred to as group health insurance or group medical claim, is a policy arranged by an employer that provides medical coverage to a defined group of individuals (typically employees and sometimes their dependents). Employers buy and manage the contract; benefits are delivered through certificates issued to members.

This article explains what corporate health insurance means in India, why businesses offer it, how the cashless and reimbursement claim routes work, common inclusions and exclusions, tax implications, and practical steps for employers and employees when selecting or supplementing cover.

What is Corporate Health Insurance?

Corporate health insurance is a single insurance contract purchased by an employer (or association) that covers a group of people under a common policy. The employer is the policyholder; employees get cover as members. The cover could be for hospitalisation, daycare procedures, select OPD or wellness services, and optional add-ons.

Policy ownership: The Employer owns the contract, and employees receive individual certificates.

Coverage period: As long as the employee is covered, good; often tied to the length of employment.

Underwriting: Group underwriting is usually easier; pre-employment checks may be minimal.

Group cover is a standard benefit offered to employees by many organisations to attract talent and reduce financial risk from medical emergencies.

Why Corporate Health Insurance Matters for Businesses

Financial security in case of medical emergencies

Group plans protect employees from heavy medical bills and lower the chance of out-of-pocket expenses that could impact salaries. For business owners, offering cover reduces the risk of payroll interruption due to financial emergencies among staff.

Employee Retention and Satisfaction

Health benefits are a key component of compensation. A strong group health plan attracts and retains talent, boosts morale, and communicates investment in employee wellbeing.

Reduced absenteeism and workplace stress

Access to care and wellness programs in a timely manner can help reduce recovery times and recurring absenteeism.

Competitive Advantage in Hiring

Companies that offer comprehensive medical benefits can distinguish themselves in tight labour markets.

Tax Benefits for Employers

Premiums paid by the employer are typically treated as a business expense (subject to tax rules). Employers should consult tax advisors for precise treatment—Section 37(1) considerations may apply.

How Corporate Health Insurance Works

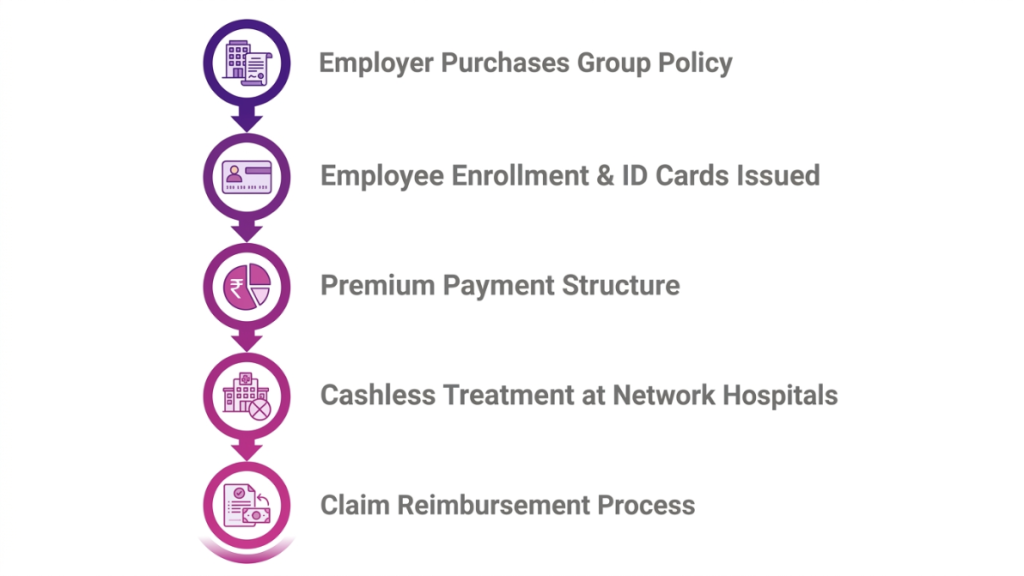

Employer Purchases a Group Mediclaim Policy

An organisation negotiates terms—sum insured, member definitions, add-ons, premium structure—and buys the policy from an insurer. The employer signs the contract and receives a master policy document.

Employee Enrollment Process

Employees are enrolled and issued insurance certificates or ID cards. Dependents may be included if the scheme allows; enrollment rules vary by insurer.

Premium Payment Structure

Depending on company policy, premium payments are either 100% paid by the employer, split between employer and employee through payroll deduction, or 100% paid by the employee. Frequency may be monthly, quarterly or annual.

Cashless Treatment Through Network Hospitals

Insurers maintain a network of hospitals. Cashless Treatment: Employees can request a pre-authorisation form from HR or the insurer for cashless treatment for planned or emergency admissions, subject to policy limits and approval.

Claim reimbursement process

In case of treatment taken outside the network or where cashless pre-authorisation is not used, employees need to submit the bills and medical documents to the insurer for reimbursement as per the insurer’s claim process and timelines.

Hospitalisation (Cashless) in India: Cashless treatment at network hospitals across the country (subject to network availability and pre-authorisation).

Pre and Post Hospitalisation Expenses: Pre and post hospitalisation investigations and treatments are normally covered for a specified number of days. Many common day-care procedures (dialysis, chemo, cataract) are covered without the need for overnight stay.

Ambulance Charges: Emergency transport cover is usually covered up to a certain limit.

Maternity and Newborn Coverage: Often available on many group plans, sometimes with sub-limits or waiting periods.

Pre-existing disease coverage: Group underwriting may reduce or eliminate the need for medical tests, although waiting periods may still apply depending on the policy.

Annual Health Check-Ups and Wellness: Preventive benefits and teleconsultation support are becoming a part of add-ons increasingly.

Types of Corporate Health Insurance Plans

Group Health Insurance (Group Medical Claim): Standard group hospitalisation cover for employees (and optionally dependents).

Group Personal Accident Insurance: Pays benefits for accidental death or disability.

Group Critical Illness Plans: Lump-sum cover for defined critical illnesses; often optional.

Employee Top-Up Health Plans: Extra coverage that starts once the basic group limit has been reached.

OPD and Wellness Cover: Additional covers or separate plans for outpatient consultation, diagnostics and preventive healthcare.

Parent / Senior Employee Coverage: Programs that cover older dependents with specific provisions.

Risks Covered Under Corporate Health Insurance

Hospitalisation Expenses: Room rent, surgeon fees, nursing, and diagnostics during admitted care.

Emergency Medical Treatment: Acute care and emergency interventions.

Surgeries and ICU Expenses: Surgical procedures and intensive care costs, subject to limits.

Chronic Illness Management: Coverage varies—some plans include chronic care, others limit support to acute episodes.

Infectious Disease Coverage (e.g., COVID-19): Most modern policies include infectious disease treatment, subject to policy wording.

Accidental Injuries: Treatment for injuries arising from accidents; separate personal accident plans may provide additional benefits.

Common Exclusions in Corporate Health Insurance Policies

- Cosmetic and elective procedures without medical necessity.

- Routine dental, vision, and non-medical consumables.

- Experimental or investigational treatments and unproven therapies.

- Self-inflicted injuries and treatment linked to substance abuse (often excluded).

- Specific waiting period clauses for certain conditions and for maternity benefits.

- Room rent limits, sub-limits for specific procedures, and caps on certain claims.

Always review the policy wording and exclusion schedule before relying on the plan.

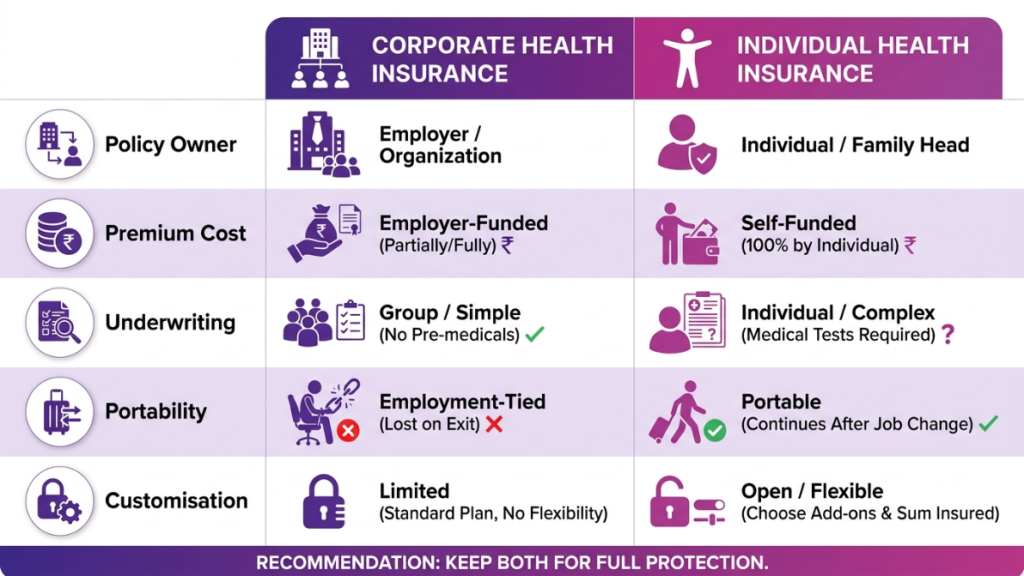

Corporate Health Insurance vs Individual Health Insurance

Both corporate and individual policies have pros and cons. Use the table below to compare core differences.

| Feature | Corporate Health Insurance | Individual Health Insurance |

| Policy Owner | Employer | Individual / Family |

| Premium Cost | Often employer-funded or shared | Self-funded |

| Underwriting | Group underwriting, often simpler | Individual underwriting; medical checks possible |

| Portability | Usually tied to employment; portability limited | Portable between jobs |

| Customisation | Limited | High (sum insured, add-ons) |

Recommendation: Even with corporate cover, many employees buy or keep individual policies or top-ups to cover family needs and ensure portability when changing jobs.

Benefits of Corporate Health Insurance for Employees

Affordable Healthcare Access: Reduced or no direct premium outlay for basic coverage.

Immediate Coverage for Pre-Existing Conditions: Group schemes sometimes offer faster acceptance of pre-existing conditions compared with retail policies.

Family Protection Options: Dependents may be covered at lower incremental cost.

Reduced Out-of-Pocket Costs: Cashless facilities and negotiated care lower immediate expenses.

Wellness Programs: Health checks, teleconsultation and preventive benefits are increasingly common.

How Much Does Corporate Health Insurance Cost?

There is no single price—premium depends on several factors:

- Company size and employee count

- Employee age and health profile

- Aggregate sum insured and per-employee limits

- Add-on benefits (maternity, OPD, critical illness)

- Historical claims experience of the workforce

- Ways companies optimise costs include higher deductibles or co-pay, wellness initiatives to reduce claims, tiered cover for senior employees and negotiating network discounts with insurers and hospitals.

How to Choose the Right Corporate Health Insurance Plan

Evaluate Workforce Needs: Understand employee demographics, dependents and common health needs.

Check Hospital Network Availability: Ensure adequate network hospitals near employees’ locations.

Compare Claim Settlement Ratios and Support: Look beyond price—consider customer service, claim turn-around and cashless approvals.

Understand Coverage Limits and Sub-Limits: Review room rent caps, procedure sub-limits and aggregate limits.

Assess Add-Ons and Wellness Benefits: OPD cover, telemedicine and preventive checks can reduce long-term costs.

Review Insurer Reputation: Claims performance, digital support and grievance redressal matter. Ask insurers for sample policy wordings, claims data and references from similar-sized companies before finalising.

Important Factors Companies Should Consider Before Buying

Company size and likely scale: small, mid-market and large employers have different negotiating power.

Employee demographics: younger workforces drive different cover decisions than older employee bases.

Budget allocation and preferred funding model: full employer funding vs shared schemes.

Industry-specific risks and remote/hybrid needs: field teams may need stronger accident cover and broader hospital networks.

Scalability: ensure policy terms allow easy addition or removal of members as headcount changes.

Looking for a flexible group health insurance plan that grows with your company? Get Expert Guidance from OmniKavvach today.

FAQs

1. Does corporate health insurance cover pre-existing conditions, and how long is the waiting period?

Many group plans cover pre-existing conditions with shorter waiting periods than retail policies, but terms vary. Check the policy for exact waiting period clauses and any condition-specific limits.

2. Who pays the premium for corporate health insurance, and can employees contribute?

Typically the employer pays but companies may share premiums with employees via payroll deductions. The chosen funding model should be clear in company policy documents.

3. What happens to my corporate health cover if I leave the company?

Coverage generally ends when employment terminates. Some insurers offer portability or conversion to an individual policy—check with HR and the insurer ahead of job changes.

4. Does corporate health insurance include maternity and mental health benefits?

Many group plans offer maternity cover and mental health support as standard or add-ons; maternity may have waiting periods and sub-limits—verify policy specifics.

5. How do I file a cashless claim and what documents are required?

Contact HR or insurer helpline immediately; for cashless treatment request pre-authorisation from the insurer. Usual documents: ID, insurer ID card, discharge summary, itemised bills, prescriptions, and medical reports.