This guide helps HR leaders and business owners in India evaluate corporate health insurance options with a decision-focused lens. It explains what corporate health insurance means, common plan types (group mediclaim, floater, individual policies, top-up and super top-up), typical cover and add-ons, the claim process, cost drivers and a practical checklist HR can use when comparing providers.

Throughout, we use India-relevant norms annual policy cycles, network hospitals, waiting periods and emphasise the operational points HR should document and verify. This is non-promotional advice; consult insurers, brokers or tax advisors for pricing and tax specifics.

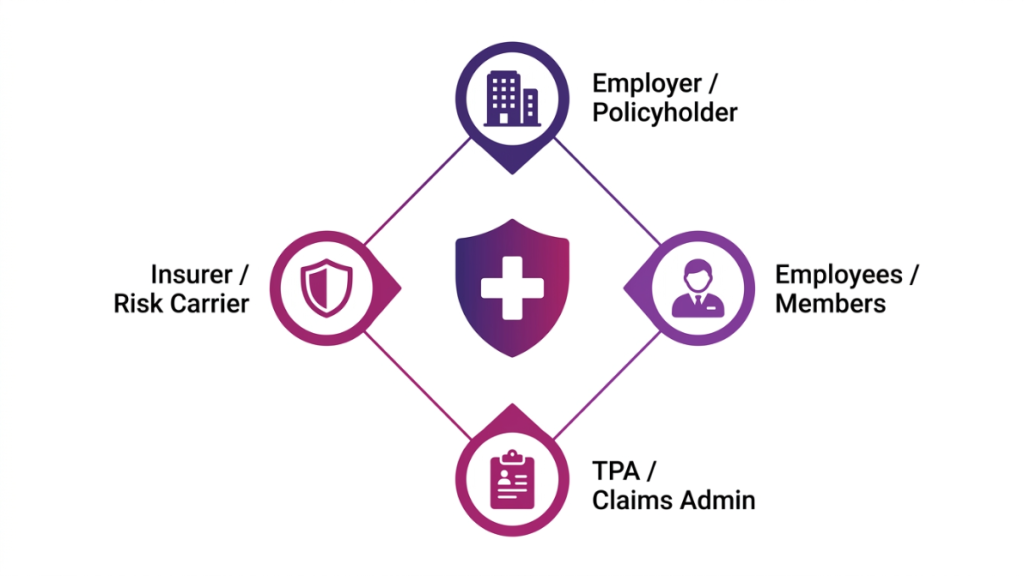

What is corporate health insurance?

Corporate health insurance (also called group mediclaim or employer-sponsored health cover) is a policy purchased by an employer that provides medical cover to employees and, optionally, their dependents. Key parties involved are the employer (policyholder), the insurer (risk carrier), employees (members), and often a third-party administrator (TPA) who handles claims and network administration.

Check out our complete guide on corporate health insurance —>

Types of corporate health insurance policies

Standard group mediclaim policies

Standard group mediclaim policies are the common employer-paid option in India. They define an annual sum insured per member (or as a floater), include in-patient hospitalisation, specified pre- and post-hospitalisation expenses and have standard exclusions and waiting periods. Renewals are annual and may change premiums based on the group’s claims experience.

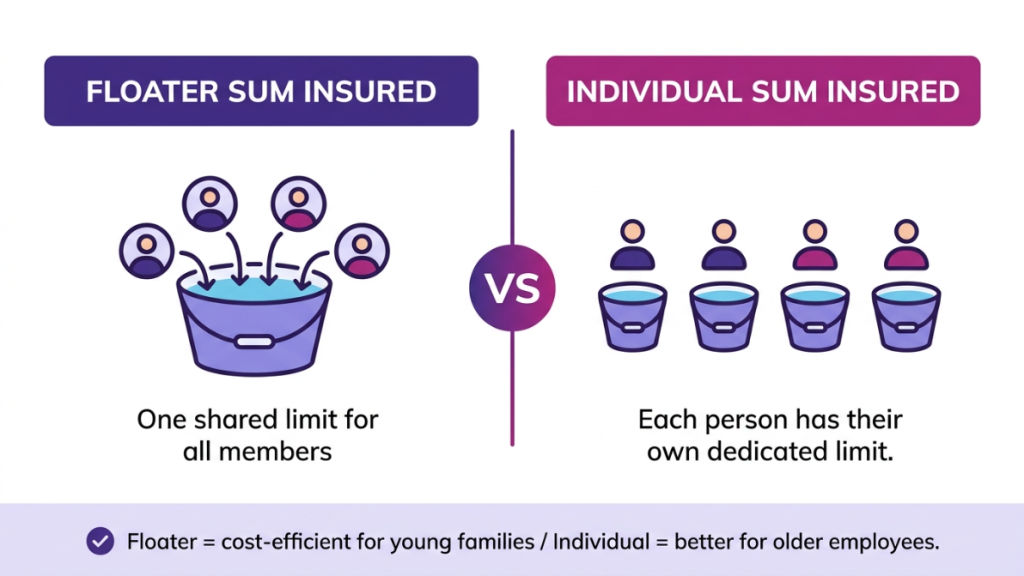

Floater versus individual sum insured

In a floater, a single sum insured is shared across covered family members or across employees in specific schemes; in individual sum insured models each covered person has a dedicated limit. Floaters can be efficient for younger, low‑claim cohorts; individual limits suit older employees or those needing family-level protection.

Top-up and super top-up plans

Top-up and super top-up plans extend cover once costs exceed a chosen threshold (the attachment point). A top-up pays per claim above the threshold; a super top-up pays once aggregate claims in a year exceed the threshold. Employers use these to protect against high-cost claims while keeping base premium costs manageable.

Individual policies arranged via employer

Employers sometimes offer negotiated individual policies or employee-purchase programs where staff buy individual cover at a group-negotiated rate. These maintain portability and personalised cover while giving employees access to preferred pricing; claims are handled like any retail policy, not as a group claim under the employer’s master policy.

Coverage, features and popular add-ons

Typical inclusions and exclusions

Corporate inpatient cover usually includes hospitalisation expenses, surgeon and anaesthesia fees, diagnostic tests, and limited pre- and post-hospitalisation care. Common exclusions are cosmetic treatments, treatments for specified illnesses during waiting periods, and elective procedures not medically necessary. Pre-existing conditions often have waiting periods (e.g., 2–4 years) which should be confirmed in the policy wording.

Popular riders and add-ons

Employers commonly add riders for OPD (outpatient) cover, maternity, newborn cover, critical illness lumpsum and dental. Add-ons make sense when specific employee needs (e.g., young families needing maternity) are common; otherwise targeted voluntary add-ons purchased by employees may be more cost-effective.

Cashless networks and room rent limits

Cashless hospitals authorised by the insurer/TPA let members receive treatment without upfront payment after pre-authorisation. Room rent capping (per-day limits and room category restrictions) is a common sub-limit that affects claim payouts and choice of hospitals HR should check the insurer’s network size and the specifics of room rent rules before finalising a plan.

Benefits for employers and employees

Recruitment, retention and employee morale

Offering health cover strengthens an employer’s benefits proposition and can help attract and retain staff. For start-ups and SMEs, a clear health benefit can differentiate offers when salary budgets are constrained. The effect on retention is strongest where benefits match employee needs—e.g., family cover for mid-career employees.

Financial protection and reduced absenteeism

Health cover reduces the financial shock of medical events for employees, which helps preserve productivity and reduces the likelihood of unpaid leave or job changes for financial reasons. Corporate plans also simplify return-to-work processes by enabling coordinated care and documentation through TPAs.

High-level tax treatment in India

Employers normally treat premiums as a business expense; employees may receive part of the premium as a taxable benefit or as tax-exempt depending on structure. Tax treatment can change with the way the benefit is structured—consult a tax advisor for specifics relevant to your organisation.

Claims, process and network hospitals

Filing a cashless claim step-by-step

- Employee/HR identifies network hospital and informs the insurer/TPA.

- Pre-authorisation form is submitted with estimated treatment details.

- Insurer/TPA confirms pre-authorisation (timelines vary but often 24–72 hours for planned admissions).

- Patient is admitted and treatment proceeds; hospital settles covered expenses with insurer directly.

- Post-discharge documents are shared and claim is finalised.

- HR typically helps with member IDs, empanelment confirmations and urgent escalations.

Reimbursement claims and document checklist

For reimbursement: submit claim form, original bills and receipts, discharge summary, investigation reports and prescriptions. Keep itemised invoices and proof of payment. Timely documentation and complete records speed processing; use the insurer/TPA checklist to avoid back-and-forth.

Common denials and how to troubleshoot

Frequent denial reasons include missing documentation, treatment falling under exclusions, claims within waiting periods, and non-pre-authorised admissions for planned procedures. Troubleshoot by reviewing policy wording, supplying missing documents quickly, escalating to the TPA claims manager, and involving HR for employer-level intervention when appropriate.

How to choose and compare plans and providers

Checklist to compare plans

- Coverage scope and sum insured (floater vs individual).

- Sub-limits and room rent rules.

- Add-ons offered (OPD, maternity, critical illness).

- Network hospital size and key hospitals in your geographies.

- Claim turnaround times and TPA support model.

- Renewal terms and typical premium increase history.

- Prioritise claim experience and exclusions over small premium differences. Document required features before inviting quotes to ensure apples-to-apples comparison.

Key insurer and policy metrics

Important metrics include claim settlement ratio, average claim turnaround time, TAT for pre-authorisation, and network hospital count. Verify these via insurer reports, TPA references and client testimonials; ask for sample policy wordings.

Questions to ask brokers and insurers

- How are renewals and premium adjustments calculated?

- Can you provide sample claim turnaround times and references?

- What are the exact waiting periods and open/pre-existing condition rules?

- Are bespoke coverage options or negotiated hospital rates available?

Record responses in proposals for internal review and scoring.

Cost, premiums and contribution models

Factors that determine premiums

Premiums depend on the employee age profile, chosen sums insured, past claims history (loss ratio), industry risk (higher-risk industries may face higher rates), and cohort size. Smaller groups can face higher volatility in pricing because a single large claim affects renewals more noticeably.

Employer versus employee contributions

Common models include fully employer-paid premiums, employer-paid base cover with employee-paid top-ups, or hybrid contributions. Contribution approaches influence employee perceptions—fully employer-paid cover is a stronger perk, while voluntary top-ups let employees choose higher protection at their cost.

Ways to control premium costs

Levers to manage premiums: increase deductibles or co-pay, add top-up/super top-up layers, implement wellness and preventive programs to lower claims, narrow voluntary benefits, and negotiate provider-rate agreements. Each lever has trade-offs between cost savings and member protection.

Eligibility, enrollment and portability

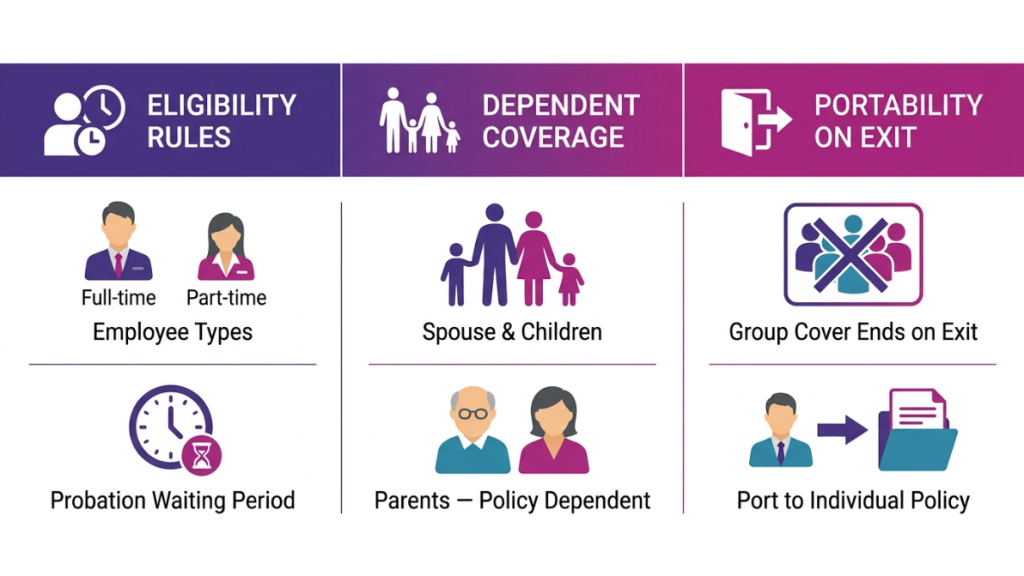

Eligibility rules and probation periods

Employers define eligibility—full-time, part-time, contractual—and may apply probationary waiting periods before new hires are covered. Document these rules clearly in onboarding materials so employees understand when benefits begin.

Dependent coverage and limits

Dependents typically include spouse and children; some policies extend to parents. Covering dependents raises premiums but improves perceived value. Be clear about limits per dependent and any family floater mechanics used.

Portability and leaving the company

Group cover usually ceases on exit. Employees can port to an individual policy to retain continuity; some insurers allow conversion offers at exit. HR should communicate exit timelines and recommended next steps to departing employees.

Wellness programs and cost control strategies

Examples of employer wellness initiatives

Practical programs: annual health screenings, vaccination drives, mental health support, fitness subsidies or partner discounts, healthy-canteen initiatives and targeted chronic-disease management. Small employers can start with low-cost screening and digital health coaching; larger employers can run integrated wellness platforms.

Insurer incentives for preventive care

Some insurers offer premium credits, lower renewal loading or wellness benefits for demonstrably lower claims or for defined participation levels. Check these incentives at procurement and align metrics you’ll track with insurer requirements.

Measuring program impact

Track KPIs such as participation rate, claims frequency and average claim size, employee satisfaction, and absenteeism. Review impact after 6–12 months and use findings in renewal conversations to negotiate premiums or design benefit changes.

Conclusion

Choosing the right mix of corporate health insurance requires balancing cost, protection and operational simplicity. Use the checklist above to prioritise features, verify claim experience and network reach, and consider complementary wellness measures to reduce long-term claims. Document eligibility, contribution rules and claim procedures clearly for employees so the plan delivers value in practice.

Secure your workforce. Strengthen your business.

Explore OmniKavach Corporate Insurance today!

FAQs

1. Can dependents be covered under corporate health insurance?

Yes. Many group policies allow spouses, children and sometimes parents as dependents—confirm limits, floater rules and premium impact with the insurer.

2. What is the difference between a floater and an individual sum insured?

A floater shares a single sum insured across covered people; individual sum insured gives each person a separate limit. Floaters can be cost-efficient for low-claim groups; individual limits provide certainty for each member.

3. How long does a cashless pre-authorisation take?

Timelines vary; planned admissions typically get pre-authorisation within 24–72 hours if documentation is complete. Emergency admissions often follow a faster on-call process but require post-submission paperwork.

4. Will group cover protect employees after they leave the company?

Typically, no group cover usually ends on exit. Employees may port to an individual policy or be offered conversion options; HR should communicate exit procedures clearly.

5. What are the common reasons for claim rejection, and how can they be avoided?

Common reasons include missing documents, exclusions, treatments during waiting periods, and non-pre-authorised planned admissions. Avoid these by reviewing policy wordings, completing documentation promptly, and following pre-authorisation processes.