Introduction

Cyber threats from ransomware and phishing to data breaches and supply-chain attacks are no longer occasional headaches. They are an everyday risk for organisations of all sizes. As a result, more businesses are looking for financial protection and incident support under the labels “cyber insurance” or “cyber liability insurance.”

In practice, these terms are often used interchangeably, but there are meaningful differences in emphasis. This guide explains both concepts, compares what they typically cover, and helps decision-makers in India pick the right approach for their exposure.

What is Cyber Insurance?

Cyber insurance is a broad term for policies designed to protect a business from the financial and operational impact of cyber incidents. It can combine first-party and third-party coverages to help organisations recover and continue operations after an attack.

Common incidents covered:

- Ransomware attacks and cyber extortion

- Data breaches exposing customer or employee information

- Business interruption caused by system downtime

- Costs to restore or recover data and systems

Key features you’ll often find in cyber insurance policies:

Incident response support: Forensic investigation and containment.

Data restoration: Costs to rebuild or recover lost data and systems.

Business interruption: Reimbursement for lost income during downtime.

Crisis management and PR: Reputation and communications support after a breach.

Cyber extortion: Coverage for ransom payments and associated negotiation expenses (subject to policy terms and local laws).

Regulatory assistance: Help with compliance and potential fines where covered.

Does cyber insurance cover ransomware payments? Many policies include cyber extortion cover, but insurers vary on sub-limits, approval processes and legal restrictions especially in India, where compliance and law-enforcement engagement may influence handling of extortion demands.

Read Our Complete Guide on Cyber Insurance in India for Businesses—>

What is Cyber Liability Insurance?

Cyber liability insurance is narrower in focus: it primarily protects the policyholder against legal and third-party liabilities arising from a cyber incident. The emphasis is on defending and settling claims brought by customers, partners, regulators, or other external parties.

Typical cover elements include:

Privacy liability: Claims from customers or employees whose personal data was exposed.

Legal defence costs: attorney fees, court costs, and settlement expenses.

Regulatory fines and penalties: Where permitted by law and covered by the policy terms.

Notification costs: Costs to notify affected parties and provide credit monitoring where required.

Third-party damages: Liability arising from supplier, client or partner losses caused by your systems or services.

Cyber liability is essential where your business processes, stores or transmits third-party data and faces potential lawsuits or regulatory action. It answers the question: “If someone sues us after a breach, who pays?”

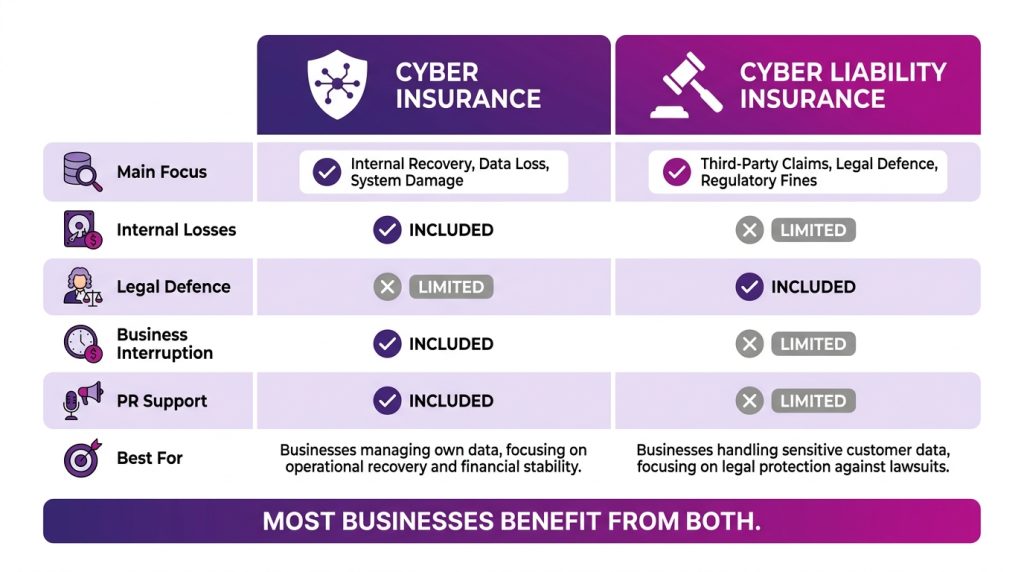

Cyber Insurance vs Cyber Liability Insurance: The Core Difference

The simplest way to think about the difference is first-party versus third-party focus. Cyber insurance (as a broad product) often bundles both first-party operational recovery and third-party liability; cyber liability insurance emphasises legal exposure and claims.

| Feature | Cyber Insurance (broad) | Cyber Liability Insurance |

| Main focus | Operational recovery + liabilities | Third-party legal and regulatory exposures |

| Covers internal losses | Yes — data recovery, business interruption | Limited — may exclude direct operational recovery |

| Legal defence & settlements | Yes | Primarily yes |

| Business interruption | Usually included | Often limited or excluded |

| Reputation & PR support | Often included | Limited |

| Best for | Businesses seeking comprehensive cyber risk protection | Businesses primarily exposed to third-party claims |

First-Party vs Third-Party Coverage Explained

Understanding first-party and third-party coverage helps you decide which policy or combination you need.

First-party coverage (your direct losses)

Data recovery and system restoration costs

Ransomware response and potential ransom payments (subject to policy terms)

Forensic investigations and breach containment

Business interruption losses lost income during downtime

PR and crisis management to limit reputational damage

Third-party coverage (liabilities to others)

Customer lawsuits for breach of privacy or negligence

Vendor or partner claims that your systems caused their loss

Regulatory fines and costs to defend investigations (where covered)

Settlements and legal defence costs

Claims process what to expect:

- Notify your insurer promptly and follow the policy’s incident reporting requirements.

- Insurer authorises or provides incident response vendors for forensics and containment.

- Documentation and forensic reports support the claim and determine coverage eligibility.

- The insurer coordinates payments for covered costs and defence/settlement where applicable.

Tip: Keep an incident response plan and documented backups; insurers often require evidence of reasonable security measures when settling claims.

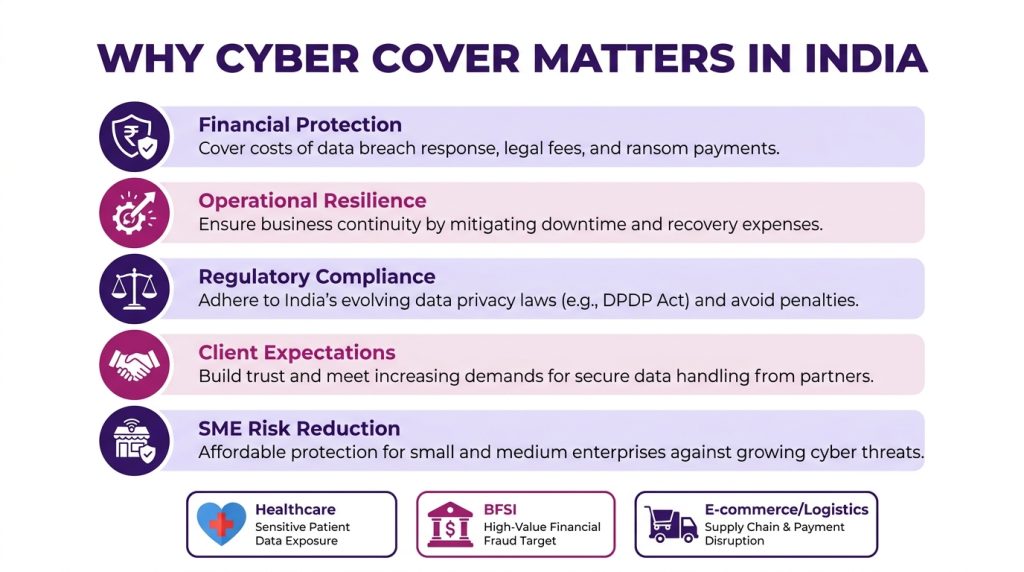

Why Businesses Need Cyber Coverage Today

Cyber incidents are costly and common. Across India and globally, ransomware frequency, phishing sophistication, and regulatory scrutiny have risen, making cyber coverage a practical part of risk management.

Key reasons to consider cyber cover:

Financial protection: Recovering systems, responding to regulators, and defending lawsuits.

Operational resilience: Business interruption cover helps manage cash flow during outages.

Regulatory compliance: Data protection laws and sector-specific rules can expose firms to fines and mandatory actions.

Client expectations: Partners and customers increasingly expect vendors to have cyber cover as a baseline risk control.

SME risk reduction: Smaller firms often lack resources for rapid incident response insurance can provide immediate expert help.

Industry-specific notes: Healthcare and financial services face higher regulatory and privacy risk; logistics and e-commerce firms should consider operational interruption and supply-chain exposures. Banks and large enterprises typically negotiate bespoke terms and higher limits; SMEs can choose standard packages with scalable limits and endorsed sub-limits

Choosing the Right Cyber Insurance Coverage for Your Business Needs

Choosing the right cyber protection is not only about comparing policy names. It is about understanding how your business operates, where your digital risks exist, and what kind of financial exposure a cyber incident could create. While cyber insurance and cyber liability insurance are often used interchangeably, the level of protection they offer can vary depending on the insurer, policy structure, and business requirements.

For businesses that rely heavily on digital infrastructure, customer databases, eCommerce platforms, cloud applications, or remote teams, a broader cyber insurance policy may offer more comprehensive protection. These policies can include support for ransomware attacks, business interruption losses, cyber extortion, forensic investigations, data recovery expenses, crisis communication, and system restoration after an attack.

Cyber liability insurance is generally more focused on third-party liabilities that arise after a data breach or privacy-related incident. This may include legal defense costs, customer notification expenses, regulatory investigations, or claims related to compromised customer information. Businesses operating in sectors such as healthcare, finance, SaaS, legal services, and eCommerce often evaluate liability-focused coverage because of increasing data privacy expectations and cybersecurity regulations.

Before selecting a policy, businesses should assess several important factors:

- The amount and type of sensitive customer or financial data stored

- Dependence on online operations and digital systems

- Potential revenue loss from downtime or operational disruption

- Industry-specific compliance and regulatory requirements

- Risks related to employees, vendors, and third-party software access

- Existing cybersecurity practices and incident response readiness

It is also important to review policy exclusions, claim limits, waiting periods, and whether coverage extends to social engineering attacks, phishing scams, or vendor-related breaches. Some policies may appear comprehensive but offer limited protection in real-world cyber incidents.

As cyber threats continue to evolve, businesses are increasingly viewing cyber coverage as part of a larger risk management strategy rather than simply an optional insurance product. Comparing coverage carefully and aligning it with your operational risks can help create stronger long-term protection against modern cyber threats.

Worried about ransomware, data breaches, or financial loss from cyberattacks? Get expert advice now!

FAQs

-

Do I need cyber liability insurance if I have general liability?

General liability typically excludes data breaches and cyber incidents. Cyber liability specifically covers privacy breaches, regulatory actions, and related legal costs—so it’s complementary rather than redundant.

-

Does cyber insurance cover ransomware payments in India?

Many policies include cyber extortion cover, but coverage depends on policy wording, sub-limits, and legal considerations. Always check approval processes and local restrictions.

-

much cyber insurance should a small business buy?

There’s no one-size-fits-all. Consider annual revenue, number of records handled, contractual requirements from customers, and potential downtime. Common entry limits for SMEs in India start at INR 25–50 lakh and scale up based on risk.

-

Will cyber insurance pay regulatory fines under Indian law?

Payment of fines depends on policy wording and local legal constraints. Some policies cover regulatory defence costs but exclude criminal fines. Verify with your insurer and broker.

-

What security controls do insurers typically require before issuing cover?

Insurers commonly ask for multi-factor authentication, regular patching, backups, endpoint protection, an incident response plan, and employee training. Controls required vary by insurer and risk profile.