What Is Travel Insurance?

A simple definition

Travel insurance is a type of short term insurance policy that will reimburse you or provide services if you have certain problems when traveling. Common policies will cover emergency medical expenses while abroad, trip cancellation or interruption, lost or delayed luggage, travel delays and emergency assistance. Plans range from single-trip policies to annual multi-trip plans for frequent travellers.

How travel insurance works

You buy a policy for a trip (or an annual plan). If a covered event occurs, you contact the insurer or their 24/7 assistance line, follow instructions (seek medical care, get police or airline reports, save receipts), and file a claim with the required documents. The insurer then reviews and reimburses eligible costs or directly coordinates services like medical evacuation.

Difference between travel insurance and regular health insurance

Travel insurance focuses on travel-related losses and short-term medical protection overseas. Regular health insurance often has limited or no cover outside your home country; travel medical cover fills that gap and typically includes emergency evacuation and repatriation, which most domestic health plans do not provide.

Who needs travel insurance?

- Leisure travellers who prepay hotels and tours

- Business travellers with non-refundable bookings or remote assignments

- Students studying abroad or on exchange programs

- Families travelling with children

- Solo travellers who want financial protection and assistance

- Frequent flyers who may prefer an annual multi-trip plan

Why Travel Insurance Matters More Than Ever

Travel risks have increased

Modern travel involves more moving parts: tight connection windows, bundled non-refundable bookings, and international medical costs that can be very high. Events such as sudden flight cancellations, lost baggage, delayed connections, or medical emergencies abroad can quickly turn a smooth holiday into significant expense and stress.

The financial impact of traveling uninsured

Out-of-pocket medical expenses: Treatment and hospital stays overseas can cost thousands of dollars.

Emergency transportation: Medical evacuation or repatriation is extremely costly without insurance.

Nonrefundable bookings: Flights, tours, and hotels often can’t be fully refunded—cancellation cover can reimburse these losses for covered reasons.

In short: a modest premium often prevents a large, unexpected bill or financial disruption to your trip plans.

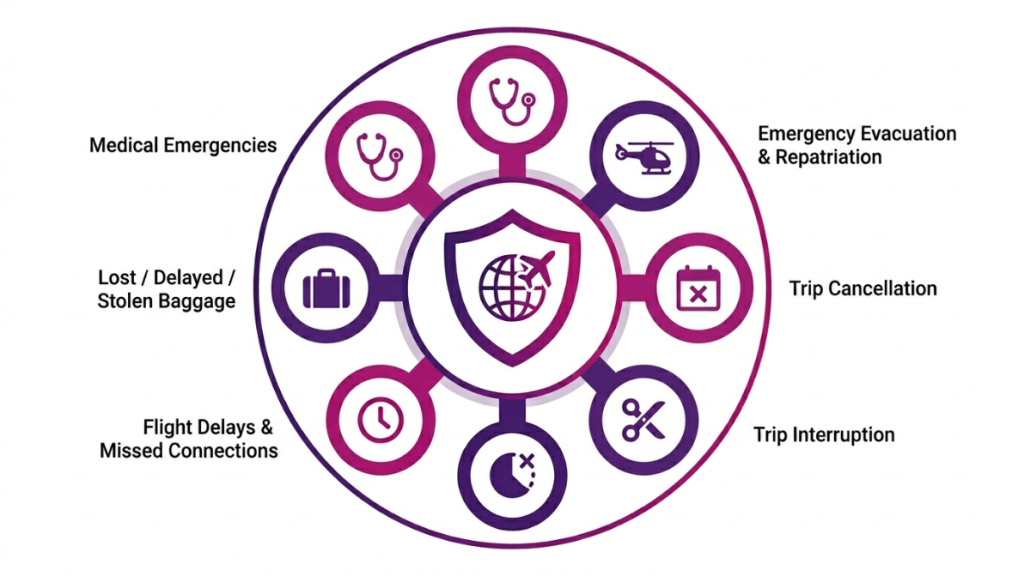

What Does Travel Insurance Typically Cover?

Medical emergencies during travel

Most policies include emergency medical expense coverage for doctor visits, hospital stays, ambulance transport, and prescriptions that arise from sudden illness or accident during the trip. Coverage limits vary check the maximum payable per incident and per trip.

Emergency medical evacuation and repatriation

If local medical facilities are inadequate, insurers can arrange and cover medically necessary evacuation to a suitable hospital—sometimes even back home. This benefit is one of the highest-cost items a travel policy can protect against.

Trip cancellation coverage

This reimburses non-refundable prepaid costs when you must cancel before departure for covered reasons (e.g., sudden illness, death in the family, or severe natural disaster at the destination). Policies list the specific covered reasons; read them carefully.

Trip interruption coverage

If your trip is cut short for a covered reason, interruption cover can reimburse unused prepayments and additional travel to return home.

Flight delays and missed connections

Many plans pay for reasonable additional expenses (meals, accommodation, local transport) when delays or missed connections occur. Keep receipts and airline delay confirmations.

Lost, delayed, or stolen baggage

Insurers reimburse essentials if baggage is delayed and may pay a set amount for permanently lost or stolen items. Policies often have limits per item and exclusions for high-value goods unless declared and insured separately.

How claims usually work: report incidents promptly (to police, airline, or hotel), keep written confirmations and receipts, call the insurer’s emergency number when medical issues arise, and then submit a claim with documentation when back home.

Common Travel Situations Where Insurance Can Help

Medical emergency in a foreign country: Insurance can pay for immediate care and, if needed, evacuation to a better-equipped facility.

Last-minute family emergency before departure: Trip cancellation cover can reimburse non-refundable costs if the reason is covered by the policy.

Airline cancellation disrupts your plans: Delay and missed-connection benefits can cover accommodation and rebooking expenses.

Lost passport or travel documents: Some policies provide support services and cash advances for emergency travel documents.

Stolen luggage during your trip: Baggage cover can reimburse essential replacements and lost items up to policy limits.

These are practical examples showing how insurance moves from theory to real financial and logistic support.

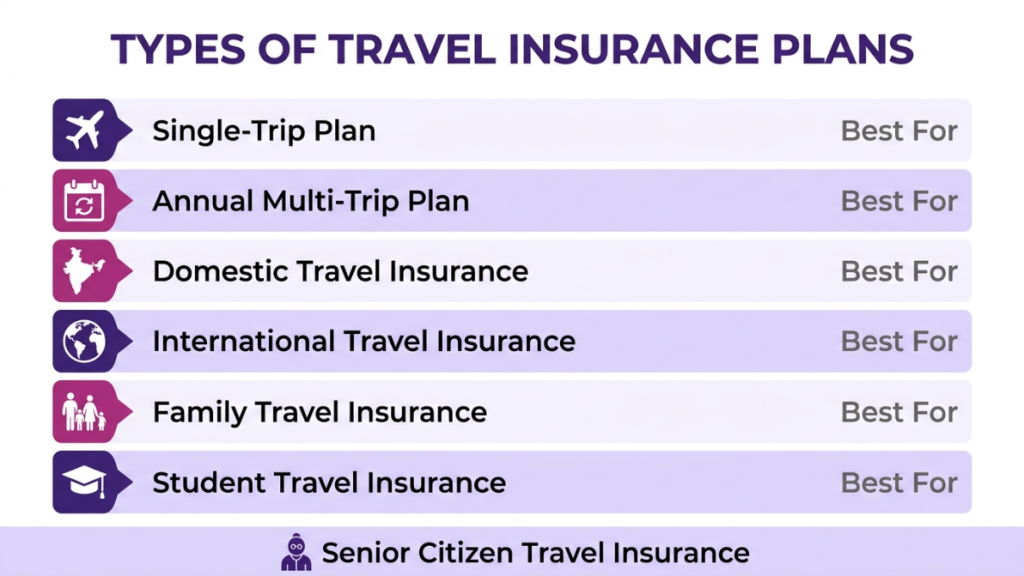

Types of Travel Insurance Plans

Choose a plan type based on travel frequency, trip length, and destination:

Single-trip travel insurance: Covers one trip from departure to return. Good for occasional travellers or a single holiday.

Multi-trip / Annual travel insurance: One policy covering multiple trips in a year is cost-effective for frequent travellers if trips are short and regular.

Domestic travel insurance: Policies focused on travel within your home country, often with lower medical evacuation needs.

International travel insurance: Designed for overseas journeys and usually includes higher medical and evacuation limits.

Family travel insurance: Covers multiple family members under one policy; convenient for family holidays.

Student travel insurance: For students studying or travelling abroad, sometimes with cover for course interruption.

Senior citizen travel insurance: Tailored for older travellers; check age limits and medical requirements.

| Plan | Best for | Typical pros |

| Single-trip | Infrequent travellers | Simple, cheaper per-trip cost |

| Annual multi-trip | Frequent flyers | Convenient, cost-effective for many short trips |

Cost depends on destination, trip length, age of travellers, coverage limits and add-ons (adventure sports, rental car excess, etc.). Compare features and limits, not just price.

What Travel Insurance Usually Does Not Cover

Pre-existing conditions (depending on policy)

Many policies exclude pre-existing medical conditions unless specifically declared and accepted, or unless you buy a policy with a pre-existing medical waiver. Always disclose chronic conditions when you apply.

High-risk activities and adventure sports

Activities such as extreme skiing, scuba diving, or motor-racing are often excluded unless you purchase an adventure sports add-on. Check the policy’s activity list and buy the speciality cover if needed.

Claims resulting from negligence

Claims caused by illegal acts, intoxication, or recklessness are commonly denied. Always follow local laws and safety guidance.

Policy exclusions every traveler should read

War, terrorism (some policies exclude these or require specific wording)

Known events at time of purchase (e.g., booking after a cruise line announced a strike)

Losses without proper documentation or timely reporting

Read the policy wording to understand exclusions — that’s the most common reason claims are denied.

How to Choose the Right Travel Insurance Policy

Follow these practical steps when selecting a plan:

Assess your destination and trip length: International trips usually need higher medical and evacuation limits than domestic travel.

Consider medical coverage limits: Look for sufficient emergency medical and evacuation limits — the single biggest risk is costly overseas treatment.

Review baggage and cancellation benefits: Check per-item limits and the covered reasons for cancellation or interruption.

Compare deductibles and premiums: A higher deductible reduces premium but increases your out-of-pocket loss if you claim.

Check emergency assistance services: 24/7 assistance with medical referrals, translation, and repatriation is invaluable in a crisis.

Tip: use a checklist to compare two to three plans side-by-side (limits, excess, exclusions, emergency number) rather than only comparing price.

When Should You Buy Travel Insurance?

Booking stage vs. last-minute purchase

Buy travel insurance as soon as you pay non-refundable deposits. Early purchase ensures coverage for events that occur after buying the policy, such as sudden illness before travel. Waiting until the last minute can leave gaps many cancellation reasons must arise after the policy start date to be covered.

Benefits of buying early

Coverage for pre-departure cancellations that happen after you’ve purchased the plan

Ability to include pre-existing condition waivers if available and purchased quickly

Some limited situations justify buying late (e.g., last-minute trips), but the safest approach is to buy at booking.

Travel Insurance Myths That Could Cost You Money

“I’m healthy, so I don’t need it”

Even healthy travellers can face accidents, travel delays, or lost baggage. The main purpose is to protect finances and logistics, not just health.

“My credit card covers everything”

Some credit cards offer limited travel protections, but they often have lower limits, narrower covered reasons, or require card payment for the whole booking. Verify the exact terms before relying solely on a card.

“Travel insurance is too expensive”

For many travellers, the premium is a small fraction of potential costs for a single large event (evacuation, hospital bills, or full trip loss). Compare coverage-to-cost rather than just premium price.

“Nothing will go wrong on my trip”

Travel plans are subject to disruption. Insurance is about managing risk — a small cost for protection and peace of mind.

Conclusion: Travel Insurance Is a Small Cost for Greater Peace of Mind

Travel insurance protects both your trip and your finances. It covers expensive risks like emergency medical treatment and evacuation, reimburses non-refundable bookings in covered situations, and helps manage the disruption of delays, lost baggage or document loss. Before your next trip, compare plans (limits, exclusions, price) and buy early—especially when you’ve paid non-refundable deposits. For details on available plans and support, review trusted providers’ service pages and their policy wordings.

Not Sure Which Travel Insurance Plan You Need?

Get an expert opinion with an OmniKavach advisor and find coverage that matches your destination, visa requents, and travel plans.

Get expert advice now!

Frequently asked questions

1. Do I need travel insurance for domestic trips in India?

Not always mandatory but recommended covers medical emergencies, missed connections, and baggage loss domestically.

2. When should I buy travel insurance before my trip?

Buy as soon as you pay non-refundable costs; ideally, when booking to protect against cancellations.

3. Does travel insurance cover COVID-19 and pandemic-related disruptions?

Some policies include pandemic coverage—check policy wording for COVID treatment, quarantine, and interruption specifics.

4. How do I file a travel insurance claim in India and what documents are required?

Intimate insurer promptly, submit the claim form plus invoices, boarding passes, medical reports, FIR and PIR where applicable.

5. Will pre-existing medical conditions be covered by travel insurance?

Declare them covered; they may be excluded, accepted with exclusion, or added via a medical waiver or rider.