Construction projects carry concentrated, expensive risk. Engineering insurance — commonly called Construction All Risk (CAR) insurance — is the policy designed to protect built works, materials and equipment from accidental physical loss and third‑party claims from project start through completion and commissioning. This guide explains what CAR covers, who needs it, common policy types and extensions, the buying and claims process, pricing drivers and typical exclusions.

What is Engineering Insurance (CAR) and why it exists

Definition and scope of CAR

Construction All Risk (CAR) is an all‑risks form tailored for construction and erection projects. It typically covers physical loss or damage to the works, materials and temporary works from the project start date until handover, often including testing and commissioning. CAR differs from standard property or general liability policies by focusing on project‑specific construction exposures.

Why projects use engineering insurance

Projects use CAR to protect capital investment, fulfil contract requirements and maintain cashflow if damage causes repair costs or halt works. It covers loss to the employer’s asset, reduces contractor insolvency risk after a major incident, and provides third‑party liability protection that many contracts and lenders demand.

What engineering insurance typically cover

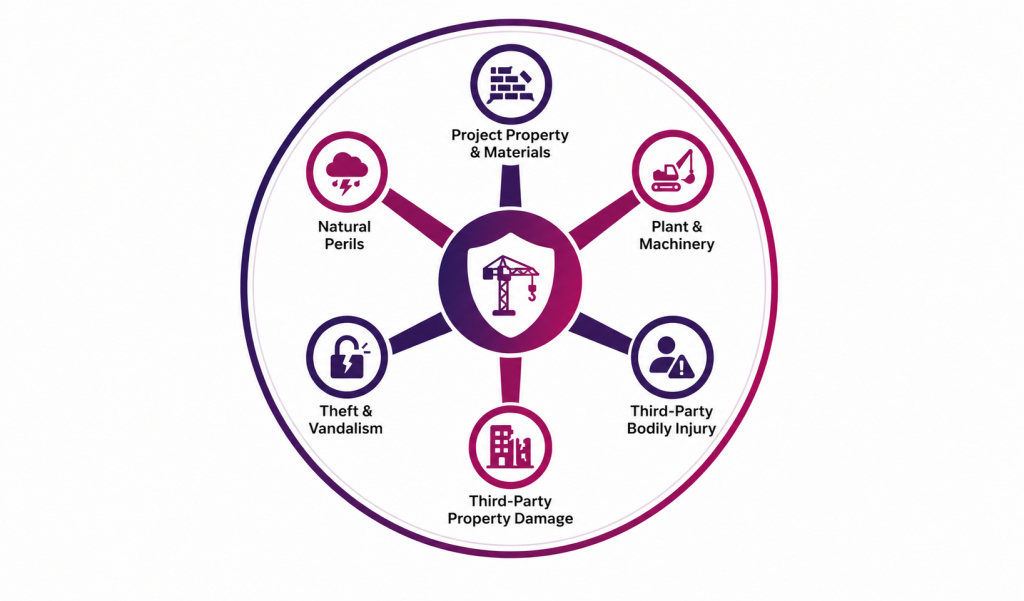

Project property and materials

CAR protects works‑in‑progress: permanent structures, temporary works, scaffolding and stored materials. Examples: if a storm partly collapses a newly erected wall or vibratory damage dislodges cladding during installation, CAR can pay to repair or replace covered items. Coverage is subject to insured perils — accidental physical damage — and policy limits or exclusions apply.

Plant, machinery and equipment

Contractors’ plant and site machinery (cranes, excavators, generators) are often covered either under CAR or a separate contractors’ plant policy. Policies may set sub‑limits and specific deductibles for plants. For high‑value mobile equipment insurers sometimes require separate schedules or valuation clauses.

Third‑party bodily injury and property damage

CAR usually includes third‑party liability for bodily injury or property damage caused by construction activities. Typical claims include pedestrian injuries from falling debris or accidental damage to adjacent buildings. Prompt incident reporting and preserved evidence are critical; insurers investigate liability and causation before settling third‑party claims.

Theft, vandalism and natural perils

Theft and vandalism are commonly included or available as extensions — important for sites with unsecured materials. Natural perils (flood, earthquake, cyclone) depend on location; some insurers include named perils only unless a specific endorsement is purchased. Always check whether perils are covered on an ‘all‑risks’ basis or must be added as named perils.

Types of engineering insurance and when to use them

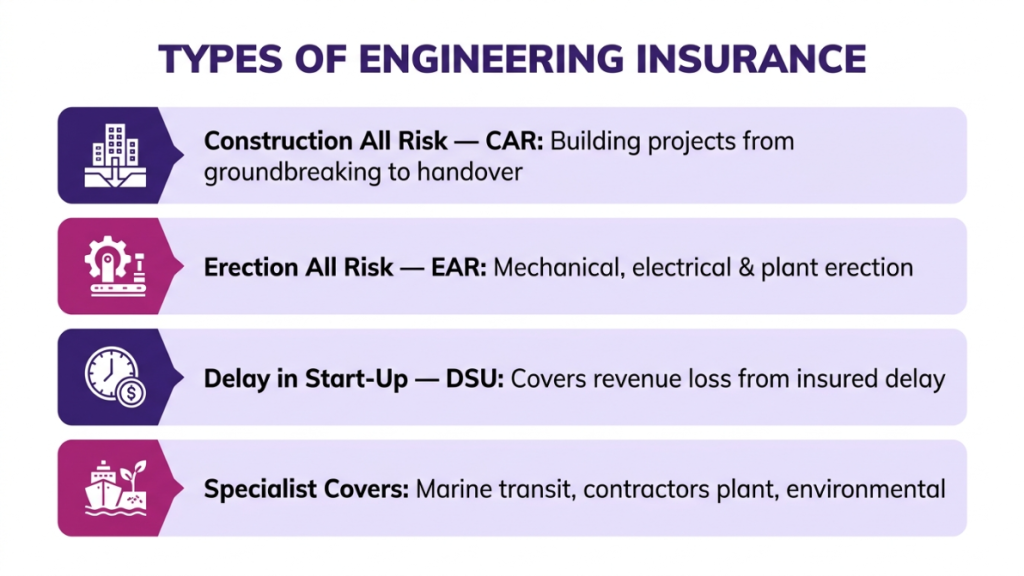

Construction All Risk (CAR)

Construction All Risk (CAR) is the baseline policy for most building projects — residential, commercial and civil works. It suits projects where physical works, materials and third‑party liability need consolidated cover from ground‑breaking to handover. For many standard builds, CAR is the first policy to purchase.

Erection All Risk (EAR) and machinery covers

Erection All Risk (EAR) focuses on mechanical, electrical and plant erection projects — for example power stations, industrial machinery and modular plant installation. EAR includes risks during lifting, testing and mechanical commissioning where delicate equipment is at risk of internal mechanical or electrical failure. Machinery breakdown insurance may be added for operational risk after commissioning.

Delay in Start‑Up (DSU) and business interruption

Delay in Start‑Up (DSU) — also called advance loss of profits — compensates for loss of anticipated revenue or additional costs when an insured physical loss delays the project’s operational start. Typical trigger: insured physical damage to a critical component requires lengthy repairs and postpones handover. DSU is commonly offered as an add‑on with defined indemnity periods and waiting periods.

Other variants and specialist covers

Specialist covers include contractors’ plant schedules, standalone third‑party liability, marine transit for imported equipment and bespoke environmental or terrorism endorsements. High‑value or unusual projects—offshore platforms, large industrial plants—typically need tailored placements and broker guidance.

Who needs engineering insurance and contractual requirements

Stakeholders who commonly need cover

Primary insureds are contractors and subcontractors who perform the works; project owners and developers are often named as insureds to protect their investment. Lenders may require borrowers to secure CAR as a condition of finance. Each party’s priority differs: contractors focus on liability and plant; owners focus on asset protection and completion guarantees. Joint insured arrangements or borrower‑owner policies are commonly used to align interests.

Contract clauses and lender requirements

Many construction contracts expressly require CAR with specified limits, named insureds and indemnity wording. Typical clauses set the policy period, minimum sums insured, endorsements (testing and commissioning) and claims notification obligations. Lenders may add conditions: loss payee status or mortgagee interest clauses. Parties should review contract wording early to confirm who must procure and administer the policy.

Deciding who should buy the policy

Owner‑procured policies give owners control and simplify claims across multiple contractors; contractor‑procured policies can be administratively simpler when one contractor carries the main risk. The decision depends on contract allocation, project size, financing and practical risk management — discuss options with legal counsel and an experienced broker early in procurement.

How engineering insurance works — buying and claims process

Getting a quote and risk assessment

Insurers typically request a project factsheet: location, contract sum (construction value), start and completion dates, scope of works, contractor details, site security and prior claims history. Underwriters may perform site surveys or request method statements for complex risks. Preparing a concise factsheet, plant schedule and risk‑control evidence (safety programs, security plans) speeds quoting and may secure better terms.

Request a tailored CAR quote from an experienced broker: preparing a project factsheet and plant schedule helps you get accurate quotes quickly.

Customising policy period and limits

Typical CAR periods run from the project start to practical completion plus a testing/commissioning window. Sums insured should reflect contract values, reinstatement costs and imported equipment value. Selecting appropriate deductibles reduces premium, but higher deductibles increase the contractor’s retained cost after a loss. Confirm whether limits are per‑loss, aggregate or subject to sub‑limits.

Claim notification and handling steps

After an incident: notify insurer as required, preserve evidence (photos, site logs, equipment serial numbers, witness details), limit site changes that could hinder investigation and provide estimates and invoices. Cooperate with adjusters during inspection and agree remediation. Common documents: contract, site diary, plant registers, supplier invoices, test reports and police reports for theft. Timely reporting and transparent records materially reduce the risk of disputes or denial.

Premiums and what drives pricing

Main premium drivers

Underwriters price around the project value and the risk profile. Primary drivers: contract sum (larger projects attract higher aggregate exposure), location (flood/earthquake zones increase rates), duration (longer programmes increase exposure), type of work (demolition or chemical works are higher risk), contractor experience and claims history, site security and storage practices. Example: a remote small project with an experienced contractor may be rated more favourably than a high‑rise inner‑city build with poor site security.

Impact of deductibles and limits

Higher deductibles typically lower premium but increase retained loss for the insured. Insufficient sums insured risk pro‑rata reductions at settlement — underinsurance can lead to proportionate claim payouts. Discuss aggregate versus per‑occurrence limits and sub‑limits for plant, transit or third‑party liability to avoid surprises at claim time.

Discounts and risk‑reduction measures

Insurers reward documented controls: secure fencing, inventory tagging, CCTV, lockable storage, staged delivery plans and formal maintenance schedules. Robust safety management, low historical loss ratios and evidence of contractor competence can attract discounts or more competitive terms — raise these points during underwriting and include mitigation evidence with proposals.

Common coverage extensions and optional add‑ons

Delay in Start‑Up (DSU)

Delay in Start‑Up (DSU) covers financial losses resulting from an insured physical loss that postpones project commissioning. DSU pays a pre‑agreed daily or monthly indemnity up to the chosen indemnity period after any waiting period. Example: a damaged turbine part delays power plant commissioning by three months — DSU can cover lost revenue or additional borrowing costs. Consider DSU where project cashflows or contractual penalties make delay costly.

Natural disaster and named‑peril add‑ons

Peril add‑ons (earthquake, flood, cyclone) are common for exposed sites. Some perils are excluded by default or limited to named peril extensions with separate rates and sub‑limits. In seismic or flood‑prone regions, insurers may require higher deductibles or engineered mitigations. Always confirm whether your policy is ‘all‑risks’ or requires specific endorsements for major natural hazards.

Theft, transit and extended liability covers

Add‑ons can include theft from site, goods in transit, and increased third‑party liability limits for urban projects. Transit cover is crucial for imported plant shipped by sea or road — insurers look for documentation (bill of lading, packing lists). Evaluate cost versus exposure; theft cover may require specific security protocols to be met.

Exclusions, limits and common claim pitfalls

Typical exclusions to watch for

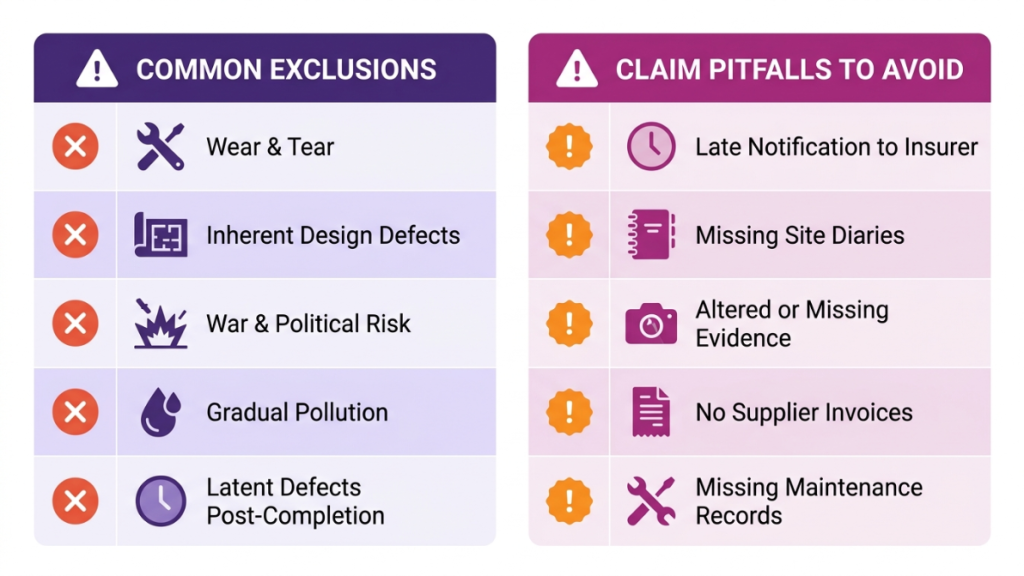

Common exclusions: wear and tear, inherent defects in design or workmanship, war and political risk, gradual pollution or contamination, and latent defects discovered after completion. Exclusions vary by policy and insurer; some can be addressed by endorsements or separate products. Clarify definitions (e.g., ‘latent defect’) and which party bears responsibility for design‑related losses.

Documentation and operational mistakes that cause denials

Late notification, absent site diaries, missing maintenance records, altered evidence and failure to follow insurer instructions commonly cause denials. Maintain daily site logs, photograph key milestones and store supplier invoices and delivery receipts. After an incident: secure the area, log witness statements, and preserve damaged components for inspection. Having a claims pack ready (contracts, plant lists, WIP valuations) speeds settlement and reduces dispute risk.

Managing policy limits and underinsurance

Undervaluing sums insured can trigger pro‑rata settlements where the insurer reduces payout proportionally. For long projects, regularly review values as work progresses and materials are added. Use agreed‑value clauses where possible and discuss staged increases in sum insured for phased projects to avoid gaps.

Related policies and complementary coverages

Public and employer liability covers

CAR’s third‑party cover is not a substitute for broader public liability or employer/worker compensation schemes. Employers’ liability and workers’ compensation (statutory in many jurisdictions) protect workforce claims; public liability can provide broader community protection. Contractors should ensure these covers dovetail with CAR to avoid gaps.

Marine, transit and storage insurance

Marine cargo and transit insurance cover materials and equipment while in sea or road transit and at offsite storage. For imported heavy equipment, overlapping transit cover and CAR must be coordinated — clarify responsibility at each handover (FOB/CIF) and ensure documents (bills of lading, insurance certificates) align.

Bundled solutions and package approaches

Brokers can assemble multi‑line packages — combining CAR, third‑party liability, contractors’ plant and workers’ compensation — to ensure consistent wording and reduce gaps. Bundled programs can simplify claims handling and may achieve better pricing through consolidated risk presentation. For complex programmes, request a broker‑led review to align limits, deductibles and cross‑policy coordination.

Conclusion

Engineering insurance (CAR and related products) is a practical risk‑management tool for contractors, owners and lenders. Start early: map contract requirements, prepare a project factsheet, and consult a broker to tailor sums insured, extensions and deductibles. Good recordkeeping and prompt claims reporting protect recoveries. For project‑specific advice, speak with a broker who specialises in construction insurance.

Frequently asked questions

1. Is Construction All Risk (CAR) insurance mandatory for every construction project?

CAR is not universally legally mandatory but is commonly required by construction contracts and lenders. Check your contract and financing terms; where required, the named insureds and minimum limits will be specified.

2. Does CAR insurance cover damage during testing and commissioning?

Many CAR policies extend to testing and commissioning if specified in the policy period or by endorsement. Confirm coverage wording and any time‑limited commissioning window with your broker.

3. What documents do I need to file a CAR insurance claim?

Typical documents: site diary, contracts, plant and materials registers, invoices and receipts, photos, witness statements, test reports and police reports (for theft). Early insurer notification is essential.

4. Will CAR insurance pay for delays in project completion?

CAR by itself pays for physical loss, not business interruption. Delay‑related financial losses are covered only if DSU (Delay in Start‑Up) is purchased — verify limits, waiting periods and triggers.

5. How long does CAR insurance remain in force?

CAR runs for the agreed construction period, often extended to include testing and commissioning. Policies can be extended for defects liability periods by endorsement.